本文源引自《金融品牌》联合出版商、《数字银行报告》首席执行官、《银行业转型》播客主持人Jim Marous在2023年10月16日发表的署名文章,采用中英双语排版,由ImmersiveTranslate提供翻译支持。

正文:

To build meaningful engagement and stem the disintermediation of relationships, financial institutions must use real-time data-driven insights that facilitate contextual interactions that display empathy across the entire customer journey.

为了建立有意义的参与并阻止关系的脱媒,金融机构必须使用实时数据驱动的见解来促进上下文交互,从而在整个客户旅程中表现出同理心。

The Digital Banking Report has consistently found that financial institutions rank improving the customer experience as the top strategic imperative that will drive success in the future. Yet, in spite of this stated priority, few organization have invested in the key components required for an enhanced customer experience or achieved the level of success desired.

《数字银行报告》一致发现,金融机构将改善客户体验视为推动未来成功的首要战略要务。然而,尽管有这样的优先事项,但很少有组织投资于增强客户体验所需的关键组件或达到所需的成功水平。

At the same time, consumers have become more demanding of what they expect from organizations across all industries. Instead of traditional forms of convenience, such as geographic proximity, consumers increasingly want to engage with companies that have advanced products that can save them time, make daily interactions more simple, and show empathy to their personalized priorities.

与此同时,消费者对各行业组织的期望也越来越高。消费者越来越希望与拥有先进产品的公司合作,而不是传统形式的便利(例如地理位置接近),这些产品可以节省他们的时间,使日常互动更加简单,并对他们的个性化优先事项表现出同理心。

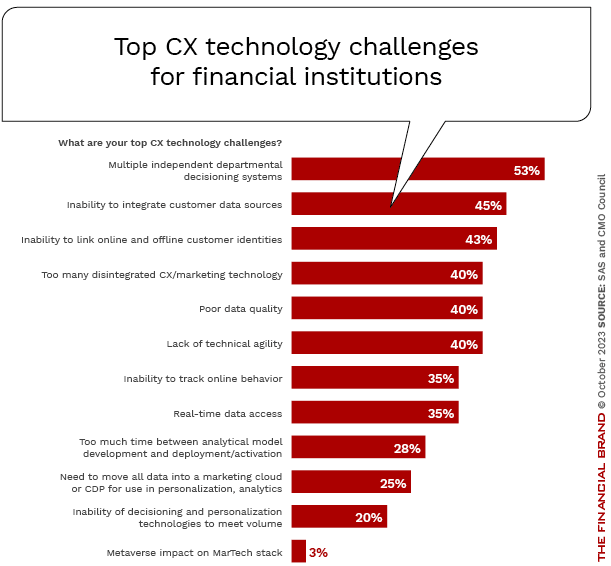

In financial services, these increased demands have come at a time of massive increases in alternative fintech and big tech competitors that are willing to deliver the highly personalized engagement levels wanted across the entire customer journey. Headwinds to delivering contextual experiences in banking also include cumbersome data silos at most legacy financial institutions, more stringent privacy laws and changes by tech companies that have marketers scrambling to get the external data needed to deliver value.

在金融服务领域,这些需求的增加是在替代金融科技和大型科技竞争对手大量增加之际出现的,这些竞争对手愿意在整个客户旅程中提供所需的高度个性化的参与水平。在银行业提供情境体验的阻力还包括大多数传统金融机构繁琐的数据孤岛、更严格的隐私法以及科技公司的变化,这些变化让营销人员争先恐后地获取提供价值所需的外部数据。

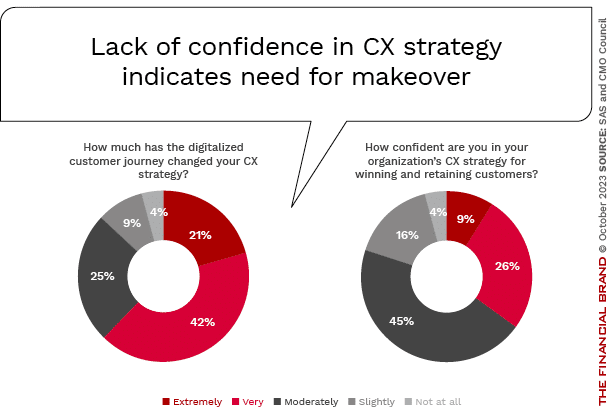

A recent study by SAS, in conjunction with the CMO Council, found that more than 60% of marketing leaders across industries say the digital customer journey has dramatically changed their CX strategy. Unfortunately, more than three-quarters of marketers aren’t very confident that their CX strategies have the ability to win and retain customers in this new environment.

SAS 与 CMO 委员会最近进行的一项研究发现,超过 60% 的各行业营销领导者表示,数字化客户旅程极大地改变了他们的 CX 策略。不幸的是,超过四分之三的营销人员对于他们的客户体验策略是否有能力在这个新环境中赢得并留住客户不太有信心。

The solution is not simple. It requires the combination of data, insights, technology and an orchestration of both digital and human channels – on a personalized level – that displays to the consumer that you know them, understand them and will reward them with frictionless engagement options and empathy in real-time. According to the research, this will require that brands:

解决方案并不简单。它需要将数据、见解、技术以及数字和人工渠道的编排相结合——在个性化层面上——向消费者展示你了解他们、理解他们,并将以无摩擦的参与选项和真实的同理心来奖励他们。时间。根据研究,这将要求品牌:

- Understand the components of customer loyalty.

了解客户忠诚度的组成部分。 - Improve their CX maturity.

提高他们的 CX 成熟度。 - Create a balance between privacy and value that creates trust.

在隐私和创造信任的价值之间建立平衡。 - Deliver on the potential of advanced marketing technology (martech).

发挥先进营销技术 (martech) 的潜力。 - Leverage AI to create increased engagement and satisfaction.

利用人工智能提高参与度和满意度。Understanding the Keys to Customer Loyalty

了解客户忠诚度的关键Marketers and consumers both prioritize certain factors when it comes to loyalty, but there are some differences. Marketers emphasize high-quality customer service, top-notch products, consistency across channels and personalized product offers and communications. In contrast, consumers prioritize high-quality products, affordability, loyalty programs and good customer service.

在忠诚度方面,营销人员和消费者都会优先考虑某些因素,但也存在一些差异。营销人员强调高质量的客户服务、一流的产品、跨渠道的一致性以及个性化的产品提供和沟通。相比之下,消费者优先考虑高质量的产品、负担能力、忠诚度计划和良好的客户服务。

Over the last several years, brands are increasingly emphasizing personalization and brand consistency over cost as a means of differentiation. While product quality and price continue to matter, they are considered essential requirements. This shift requires marketing to increase the use of data, advanced technology and artificial intelligence to deliver on other aspects of the customer experience that drive loyalty.

在过去的几年里,品牌越来越强调个性化和品牌一致性而不是成本作为差异化手段。虽然产品质量和价格仍然很重要,但它们被认为是基本要求。这种转变要求营销部门增加对数据、先进技术和人工智能的使用,以提供提升忠诚度的客户体验的其他方面。The SAS report states that consumers may not place personalization at the top of their loyalty factors because the basics are being met by many organizations. Alternatively, most consumers may not view contextual engagement or empathy as part of the definition of “personalization,” but as a component of high quality products. Either way, financial institutions must better understand the psychology of their customers to bridge the gap between what they say and what they do.

SAS 报告指出,消费者可能不会将个性化置于其忠诚度因素的首位,因为许多组织都满足了基本要求。或者,大多数消费者可能不会将情境参与或同理心视为“个性化”定义的一部分,而是将其视为高质量产品的组成部分。无论哪种方式,金融机构都必须更好地了解客户的心理,以弥合他们所说和所做之间的差距。Lack of CX Maturity Challenges Marketers

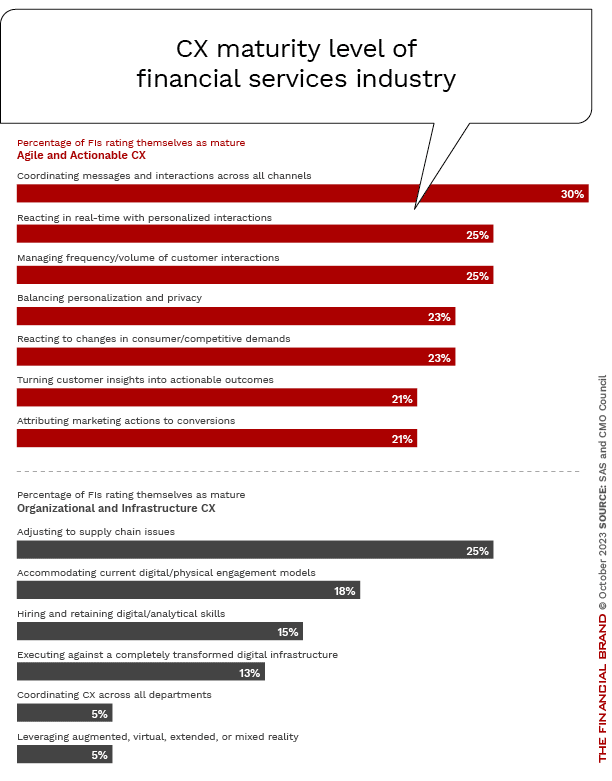

CX 成熟度的缺乏给营销人员带来了挑战The research makes a clear case that even after massive digital acceleration, many financial institutions still struggle to realign customer experiences for the digital world. A significant percentage of banking marketers say the digitization of customer journeys dramatically changed their CX strategies. However, more than half lack confidence that their revamped strategies can actually retain and engage customers.

该研究清楚地表明,即使在大规模数字化加速之后,许多金融机构仍然难以为数字世界重新调整客户体验。很大一部分银行营销人员表示,客户旅程的数字化极大地改变了他们的客户体验策略。然而,超过一半的人对他们调整后的策略能否真正留住和吸引客户缺乏信心。

This highlights an imperative for banks and credit unions to reimagine how they deliver experiences amidst surging disruption. Today’s consumers demand omnichannel convenience, personalized real-time engagement, and mobile-first, digitally integrated experiences. Legacy financial institutions that cannot deliver on these digital imperatives risk losing ground to more agile competitors.

这凸显了银行和信用合作社必须重新思考如何在激增的干扰中提供体验。当今的消费者需要全渠道的便利性、个性化的实时参与以及移动优先的数字集成体验。无法满足这些数字需求的传统金融机构可能会输给更敏捷的竞争对手。Banks adept at deriving actionable intelligence from customer insights and nimble enough to act quickly can foster much deeper consumer relationships through advanced engagement. The key to seizing these CX possibilities lies in fully utilizing data, analytics and technology to revolutionize how engagement is supported.

银行善于从客户洞察中获取可行的情报,并且足够灵活,能够迅速采取行动,可以通过高级参与来培养更深层次的消费者关系。抓住这些客户体验可能性的关键在于充分利用数据、分析和技术来彻底改变参与的支持方式。

To unlock the speed and agility demanded in digital markets, banks must reinvent infrastructure from the ground up. Transitioning core platforms to the cloud will provide the elasticity and resilience needed for always-on, data-driven customer experiences. APIs and microservices will also prove critical – allowing more nimble development of CX capabilities that can snap into an open architecture.

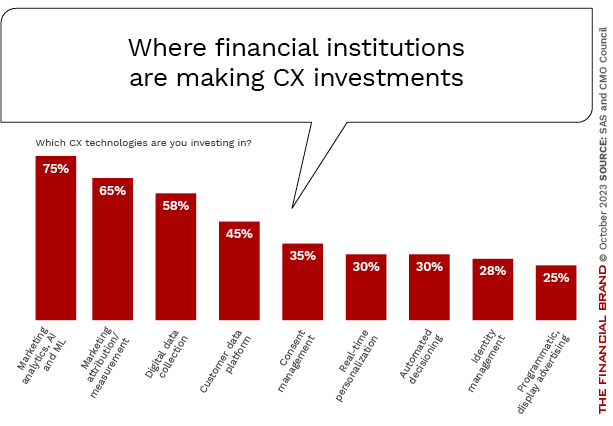

为了释放数字市场所需的速度和敏捷性,银行必须从头开始重塑基础设施。将核心平台过渡到云端将为始终在线、数据驱动的客户体验提供所需的弹性和复原力。 API 和微服务也将被证明至关重要——允许更灵活地开发可融入开放架构的 CX 功能。While 75% of financial institutions are investing heavily in artificial intelligence and machine learning to elevate CX, only 45% are focusing investment on foundational data platforms, and only 30% are investing in real-time personalization. This risks initiatives underperforming expectations, with AI unable to draw connections from fragmented sources and engagement suffering due to lack of contextual engagement.

虽然 75% 的金融机构大力投资人工智能和机器学习以提升客户体验,但只有 45% 的金融机构将投资重点放在基础数据平台上,只有 30% 的金融机构投资于实时个性化。这可能会导致举措表现不佳,因为人工智能无法从分散的来源中建立联系,并且由于缺乏上下文参与而导致参与度受到影响。

The research strongly signals that banks’ AI ambitions will necessitate higher investments across virtually all CX technologies. Combining rich, holistic data sets with AI’s analytical powers will enable next-level intelligence – from predictive behavioral modeling to ultra-personalized recommendations. Data, AI and effective deployment of solutions across the customer lifecycle must evolve in lockstep for CX gains.

该研究强烈表明,银行的人工智能雄心将需要对几乎所有客户体验技术进行更高的投资。将丰富、全面的数据集与人工智能的分析能力相结合,将实现从预测行为建模到超个性化建议的新水平智能。整个客户生命周期中的数据、人工智能和解决方案的有效部署必须同步发展,才能实现客户体验收益。Balancing Privacy, Personalization and Value Transfer

平衡隐私、个性化和价值转移SAS found widespread consumer distrust in how brands handle personal data and privacy. Over 65% of consumers feel they lack control over how brands use their data. More than half believe brands fail to keep them informed on data usage or disclose security breaches transparently.

SAS 发现消费者普遍对品牌处理个人数据和隐私的方式不信任。超过 65% 的消费者认为他们无法控制品牌如何使用其数据。超过一半的人认为品牌未能让他们了解数据使用情况或透明地披露安全漏洞。Despite these concerns, privacy ranks lower among factors that currently drive brand loyalty. In fact, over 80% of consumers are willing to share personal data in exchange for something of value like rewards or personalized offers. This willingness has risen notably since before the pandemic, according to the research.

尽管存在这些担忧,但在目前推动品牌忠诚度的因素中,隐私的排名较低。事实上,超过 80% 的消费者愿意分享个人数据以换取奖励或个性化优惠等有价值的东西。研究表明,自大流行之前以来,这种意愿显着上升。The key is offering value in return for data. When consumers don’t see value from data collection, they resent the lack of control and are primed to act against brands. To address privacy concerns while delivering personalized experiences, brands need adaptable customer data platforms. These can integrate data silos, manage consumer consent, and synchronize online and offline data. Agile data systems that rapidly incorporate new sources will be critical.

关键是提供价值以换取数据。当消费者看不到数据收集的价值时,他们会对缺乏控制感到不满,并准备对品牌采取行动。为了在提供个性化体验的同时解决隐私问题,品牌需要适应性强的客户数据平台。这些可以集成数据孤岛、管理消费者同意并同步线上和线下数据。快速整合新来源的敏捷数据系统至关重要。First-party data strategies are also essential because third-party data options are declining. Brands must focus on capturing and applying consumer permissioned data to drive differentiation through relevant experiences. Handled responsibly, first-party data powered by value exchange will be pivotal for increased customer engagement.

第一方数据策略也至关重要,因为第三方数据选项正在减少。品牌必须专注于捕获和应用消费者许可的数据,以通过相关体验推动差异化。如果以负责任的方式处理,由价值交换提供支持的第一方数据对于提高客户参与度至关重要。AI is the Gateway to CX Excellence

AI 是通向卓越 CX 的门户The SAS research makes a case that AI is the tool that can help both financial institutions and customers. “On the customer side, AI can serve up better, more rewarding experiences. On the marketing side, AI can produce algorithmically driven attribution that ties CX actions to business outcomes,” the research states.

SAS 研究证明人工智能是可以帮助金融机构和客户的工具。 “在客户方面,人工智能可以提供更好、更有价值的体验。在营销方面,人工智能可以产生算法驱动的归因,将客户体验行为与业务成果联系起来。”该研究指出。AI can predict the near future with a high degree of confidence and power real-time communication that is highly personalized. This helps marketers get out in front of CX and deliver the right experience or content to the right person at the right time in the customer journey.

人工智能可以高度自信地预测不久的将来,并支持高度个性化的实时通信。这有助于营销人员站在客户体验的前面,在客户旅程中的正确时间向正确的人提供正确的体验或内容。

More than ever, investing in AI/ML is marketing’s top priority for addressing the digital journey. Predicting behavior and omnichannel personalization are AI’s top uses. This aligns with pre-pandemic research showing increasing reliance on AI-powered intelligent systems for engagement.

投资人工智能/机器学习比以往任何时候都更成为营销应对数字化旅程的首要任务。预测行为和全渠道个性化是人工智能的主要用途。这与大流行前的研究相一致,研究表明人们越来越依赖人工智能驱动的智能系统进行参与。AI also enables more accurate attribution by uncovering patterns between touchpoints and outcomes. Algorithmic attribution identifies which interactions and journeys actually drive conversions. AI analyzes paths of both converting and non-converting customers to pinpoint what triggers desired outcomes.

人工智能还可以通过揭示接触点和结果之间的模式来实现更准确的归因。算法归因可以识别哪些交互和旅程真正推动了转化。人工智能会分析转化客户和非转化客户的路径,以查明是什么触发了期望的结果。AI’s analytical prowess is critical for elevating CX relevance and optimizing marketing spending. By predicting needs, personalizing engagements, and clarifying attribution, AI can help financial intitutions maximize impact across the customer lifecycle.

人工智能的分析能力对于提高客户体验相关性和优化营销支出至关重要。通过预测需求、个性化参与和澄清归因,人工智能可以帮助金融机构在整个客户生命周期中发挥最大影响力。